cpf

1

A Singapore Government Agency Website

Back to home

Updated by CPF

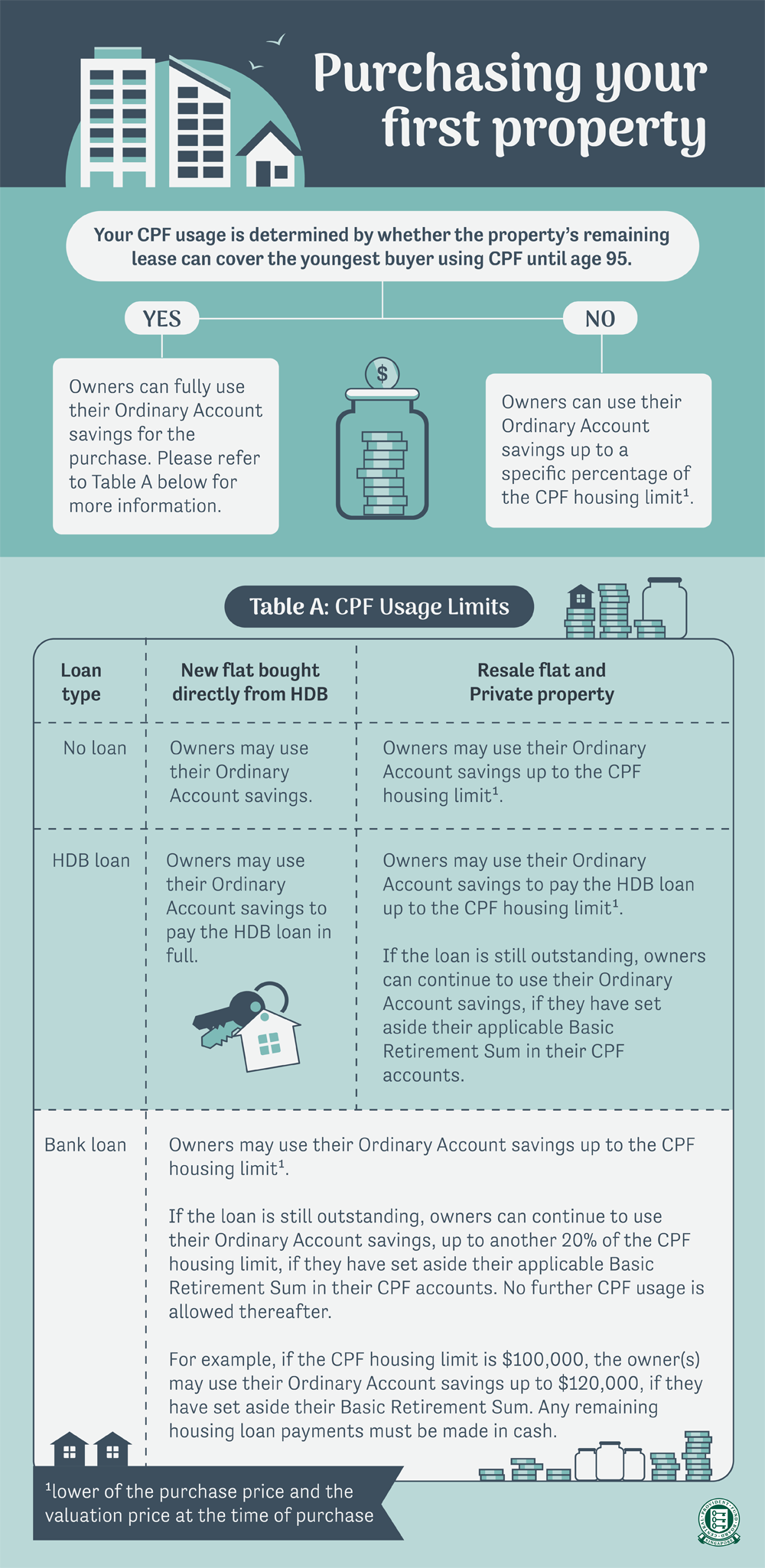

How much CPF savings can I use for my property purchase?

The amount of CPF Ordinary Account (OA) savings you can use depends on:

- Remaining lease of the property

- Type of property

- Loan type

- Whether it’s your first or subsequent property

Note: For members age 55 and above, your Basic Retirement Sum (BRS) is half of your Full Retirement Sum (FRS) which depends on the year you turn 55 and will remain the same for life. For members below 55, your BRS is half of the prevailing FRS in the year.

You can use our CPF Housing Usage Calculator to determine the total amount of CPF savings that you and your co-owner (if any) may use to buy your property.

Purchasing your second or subsequent property

You can only use your OA savings after setting aside the BRS or FRS (refer to Table B), up to the CPF housing limit of your property.

Table B: Amount to set aside

| Property Ownership | Amount to set aside |

|

Buyer has at least one property that can last him till age 95 | BRS* |

| Buyer has no property that can last him till age 95 | FRS* |

* Savings from your Retirement Account or Special Account and OA can be used to meet the requirement.

For comprehensive information about using your CPF savings for property purchases, please refer to the Terms and Conditions.

This information is sourced from CPF.

Related questions

Need more help?

Describe your issues to us.